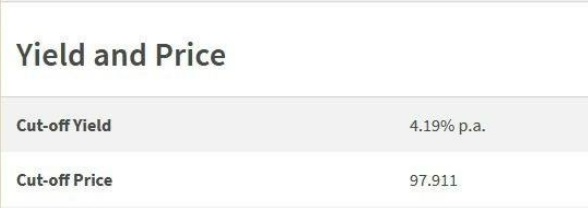

The auction results for the latest 6-month T-bill (Issue code: BS22121F) was out yesterday and the yield has finally breached the psychological 4% number.

Having slept on it for a night, here are some quick thoughts on whether you should buy the next issue or continue to wait.

Wait

Inflation remains sky-high and the Fed is still going to raise rates during their next few meetings. Personally, I think we will see T-bills yielding 5% soon, maybe in early 2023. That, honestly, would be a sight to behold.

I could be wrong, but 5% risk-free rates should be the peak or thereabout in Singapore. I am not able to fathom what would break in the economy if we see 6% risk-free rates that stays elevated for a year or two. Folks who are leveraged to the hilt for their properties, please look away.

Even at 5%, I think the prices of some REITs would drop like grapes. I mean, if you are just investing for yield, how attractive would Parkway LIFE look right now? At current prices, it is yielding less than 4%. Why not avoid the REIT and park it in a T-bill?

Of course, if you think rates will be this high only for a short period of time, then the discount in REITs would suddenly seem very attractive. It might be worthwhile then to keep the dry powder, wait for a flash crash and when the time comes, add on your REIT exposure.

Even if you are more conservative and would like to avoid equities during this period, it might be prudent to wait for a T-bill or SGS with a longer duration (12 months, 2 years or even 5 years), especially for your cash. Then, you get to lock-in a good rate for a longer period and there is less effort/anxiety to keep reinvesting the funds every half a year in 6-month T-bills.

Buy

I understand that all of us would like to allocate a portion of our savings to stable, risk-free instruments.

Especially if one is near retirement and with significant idle funds in CPF OA. In that case, I personally think it is time to act, familiarise yourself with the application and bidding process and allocate at least a small tranche in the next 6-month T-bill issue. Because there is a non-zero chance that the Fed might pivot soon and this is indeed the peak rate or thereabouts. Who knows?

In a previous post debating if we should invest CPF funds in T-bills (widely circulated), using an example where $50,000 of CPF OA funds was invested in a 3.77% 6-month T-bill. the arbitrage value (additional return compared to leaving the savings in the CPF OA account) was around $200. If we had managed to invest $50,000 in the latest 4.19% 6-month T-bill, the arbitrage would increase to $300.

That probably justifies a trip with my mother-in-law down to a local bank to kickstart this CPF OA to T-bill process.

Good to test the water with a relatively small amount first. So that if rates do go up to 6%, you are ready to load your CPF cannon and drain your CPF funds!

Read also:

7 Things You Need To Know Before Investing Your CPF Savings In T-Bills Or SGS Bonds

Subscribing For This Month’s Singapore Savings Bond (SSB)

Singapore Savings Bonds: A.K.A LKY Bonds

Thanks for reading.

If you enjoyed this article or found it useful, do subscribe to my blog via email to receive notifications of new posts.

Do follow me on these channels for updates too!

Thanks for the support!

Personally, I am irritated by ads and pop-ups so I do not use any of them on this blog too.

There is an issue of information not flowing to everyone. If everyone is rational, they would have moved most of their cash and CPF OA into Singapore T bills. Banks would be forced to increase home loan rates (SORA) and the Singapore government will be forced to top up cash to support CPF HDB loans at 2.6% while paying T bill subcribers 4.19%; this will bleed the Singapore government into billions of dollars in deficit.

Alas, this is unlikely to happen. However, if it does, then its true REITs and housing loans will be down like a wave of card. But only if information flows to everyone, which does not happen in reality

yes, perfect information does not exist. This is also the reason why there is arbitrage in this world. Another good example where information does not flow is not everyone practices CPF SA shielding at 55. That is probably a more stark example when the passive person really loses out.