I do not know about you but there is a surprising lack of CPF posts during this transition from Year 2025 to Year 2026. Or maybe it is just my algorithm.

My theory is that with the stellar stock returns in most markets, posting CPF interest seems a bit… underperforming? Not very guru-like. It is all about beating the market, isn’t it?

CPF Top Ups Are Tempting

However, I took a special interest in CPF recently. Even though my CPF balances are very humble, I was actually pleasantly surprised that the interest paid out on 1st Jan is actually quite close to the median monthly wage. So pleasantly surprised that I actually thought about topping up my CPF MA account. Only to be dismissed by the Mrs who reminded me of the illiquidity of CPF funds. LOL.

Well, as a caveat, I liquidated my UOB One Account (1.9% is pathetic) so there is $150k sitting around. Putting this amount into the market at these valuations does appear abit reckless. So I pondered over options like repaying my 2.6% HDB mortgage loan, SSBs at 2.25% or topping up CPF MA/SA at 4%.

Especially after seeing a post like this from CPFB that subconsciously tells me that I am far behind.

I definitely do not expect to have $300k in my CPF account when I turn 50.

But then, I start to wonder what is the asset allocation like for these “average” Singaporeans. Are they on course for an early retirement and what kind of safe withdrawal rate can they expect?

Allocation Split And Withdrawal Rates

I mean, do these individuals really also have a 700k stock portfolio to ensure a 70/30 allocation split? Unlikely. What’s the odds most of them are financial bloggers, hmm?

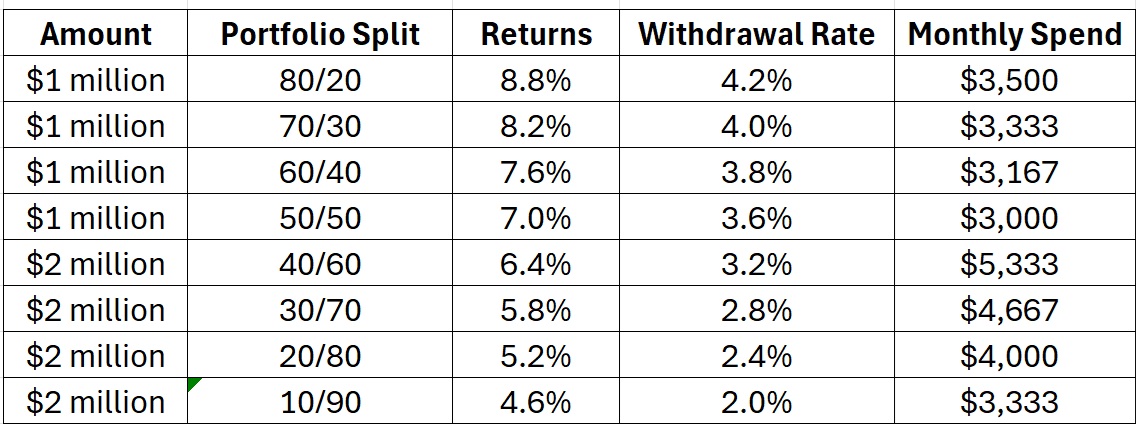

The basis for the 4% safe withdrawal rate assumes a large stock allocation to derive high single-digit returns. So I played around with some figures and permutations and came up with the table below to roughly project the withdrawal rates for different allocation rates. I assumed a 10% return for stocks and a generous 4% for CPF/cash-like instruments.

Some reflection points on the table above:

- Even from my perspective, after including CPF funds, I find it very difficult for an individual to achieve a 70/30 split. The equity portion would appear to be too heavy for my appetite. I am probably aiming for 60/40 in the long run although 70/30 would be ideal.

- For example, my wife is helping my in-laws to have more exposure in equities and she is struggling to push above 25/75 for them.

- A 4% return is obviously not enough to sustain a 4% withdrawal rate. For a 20/80 split, an individual would need $2 million to withdraw $4,000 a month at a 2.4% withdrawal rate.

- The second and the last row produces a similar monthly spend although the portfolio is twice the size in the last row. It is always about tradeoffs. There is a price to pay for more certainty and lower volatility in the form of having to save a larger sum of money.

Conclusion

CPF top ups can actually be a great option for a traditional retirement at age 65 or even 60. I can imagine a 65 year old with 500k CPF balances and another 500k in stocks comfortably spending $3k to $4k a month for the next 20 to 25 years.

As for me who wants to have the option of a SWR of 3.6% before age 50, I would probably have to split the $150k into a 60/40 or even a 70/30 allocation. Yes, continue resisting the siren call of CPF top ups.

Thank you for reading.

Mrs 15HWW and I are tutors teaching English, Math and Science from our home in Punggol. If you are staying in the Northeast and looking for a tutor for your child, do approach us!

Same.. I am resisting too because of the illiquidity concerns.

I topup my MA by 3.5k to the new BHS. Couple of reasons,

1. tax relief.

2. I’m 56yo in 2026, RA was at FRS when I hit 55. if MA is not topup, salary contribution will still go to MA. After topping up, all the CPF contribution will flow to OA which I can withdraw anytime.

3. I treat MA like a 4% FD. Interest will flow to OA every Jan.

Topping up depends on individual situation, no right no wrong.

Can share where u put the 150k from UOB 1? I am facing the same issue.