After more than a year blogging about personal finance and investments, I am surprised that something as important as asset allocation has never been directly addressed in any of the posts. To be fair, I have talked about the importance of holding some cash so that I could sleep better at night. But that’s really just scraping the surface of this important issue.

Many studies (an example here) have shown that for most investors, asset allocation plays a bigger factor in returns as compared to the individual stocks that we select in the portfolio. And since I do share my portfolio of passive income, not going deeper into asset allocation does come across as a tad irresponsible. 😳

So here’s a closer look at this topic in greater detail:

====================

Why do we need an asset allocation strategy?

In case you’re lost, equities/stocks is just one of many asset classes. There’s hard assets (gold, silver etc), cash, bonds and real estate*, just to name a few.

And historically, equities have outperformed the rest of the asset classes. Therefore, theoretically, you could put 100% of your investable assets into the STI ETF or a global ETF and forget about it till the day you need the money.

However, there’s the danger that you might just need the money in the year the stock market suffers a bad crash (>30% fall) and wipe out your portfolio. And even if the crash occurred in earlier years, there’s every chance you could bail out, sell at a low and miss the subsequent rally. After all, most people tend to overestimate their risk tolerance.

And this is where the other less volatile asset classes comes in.

Main asset allocation strategies

There’s two major ones and I shall offer a brief description on them.

a) 60/40 equities-bond portfolio

This is the most traditional and probably also the most common asset allocation strategy. And for good reason. Many studies have shown that bonds have been resilient (or even performing well) when stocks tank.

Therefore if the stock market tanks by 30%, with bonds as a cushion, the overall loss might only be in the region of 15%, which is much more palatable. One would then be less shocked by the loss and more inclined to persist with long-term investing.

The 60/40 ratio could be adjusted depending on your risk profile and age and if one rebalances the portfolio at the end of the year, he could take advantage and sell the asset class that has been performing and vice-versa. Asset classes show strong evidence of reverting to the mean.

In Singapore, government bonds aren’t that attractive so you could replace the fixed income asset with cash for a simple asset allocation strategy.

b) Permanent Portfolio

25% each in these 4 asset classes: equities, hard assets, cash and bonds.

With less exposure to equities, this “lazy” portfolio would really be reassuring to the very risk-averse. I would expect the maximum yearly decline to be at most 10%?

And amazingly, such a portfolio wouldn’t have performed too badly in the last decade, judging from this article from BigFatPurse.

My Strategy

Most asset allocation strategies work in the long run and I hope that by sharing how I do it and the reason behind the formulation, you are able to select a suitable strategy for yourself. Here’s mine:

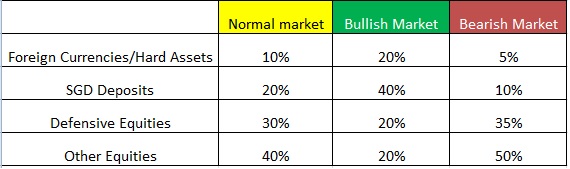

- I agree it’s impossible to time a market accurately in the sense that one can’t always buy at the lowest price and sell at the highest price over a short period of time. (I mean a few years here.) However, I believe that allocating more to equities when valuations are low and vice versa can be a profitable strategy for me.

- I think equities is too broad as an asset class and divided it into two. My hope (or wishful thinking?) is that the defensive equities that I have picked are able to function as high-yield bonds i.e. share price generally more resilient. Some examples in my portfolio that come to my mind would be Singtel, Vicom, the two healthcare Reits, ST Eng and maybe Semb Corp.

- I personally don’t really advocate hard assets as investments and prefer to keep it simple without foreign currencies. However, I am a little paranoid and these assets serve as a small hedge (some silver coins to pay for a boat out?) in case a small country like ours gets into trouble. 🙁

====================

By no means am I trying to encourage you to follow my strategy. But I hope to get you thinking because in the end, it’s about choosing and adapting a strategy to suit your own unique situation/risk tolerance/preferences.

*Real estate was excluded in this discussion as most Singaporean home owners have a significant chunk of net worth in this asset class which is going to skew the numbers for the other asset classes. And from the asset allocation point of view, I wouldn’t encourage most people to invest in a second or third property because this would literally mean an allocation of >90% in real estate or taking on risky leverage. Unless one has really deep pockets which I am sure most of my readers don’t. (Seriously, if you are, can email me why you are reading this blog?!)

Hi 15hww

Asset allocation is generally an important play that many retail investors (including myself) are not keeping a close look at unless you are assets manager by training.

But im beginning to look at them slowly but surely now especially if the market continues to be bullish as what we’ve seen for past couple of years.

Hi B,

To be honest, I think most retail investors can benefit alot from having an asset allocation. Asset allocation is much simpler to learn than picking stocks and limiting one’s exposure to “more risky” assets could be the difference between exiting early or staying vested long-term.

Most investors follow some internal guidelines but it’s sometimes good to write it out in black and white to better restrain yourself.

As the portfolio gets bigger and bigger, my admirations really go out to those who have been through a bear market before and can still remain ~100% invested in the market. Even though I still don’t think the local market is overvalued, I am pretty sure we are not going to be insulated if the frothy US market tumbles.

asset allocation is seldom talked about because every one look at it as cash or stocks.

they fail to understand that you will be pretty fucked psychology if you failed to grasp how important pscyhogloy is.

you plan is challenging because….. how the hell you tell a bull or bear market that is emerging!!!

Hi Kyith,

Actually using cash and stocks as two asset class could be good enough for a simple to execute strategy in Singapore, especially if there is CPF contributions.

Bullish or bearish is actually pretty obvious on hindsight but have to admit going forward isn’t straightforward. I guess one way to do it would be using simple P/E ratio to look at valuation metrics. Bullish is when P/E of STI is near 20, fair is when it’s between 10 to 15 and bearish below 10?

How are you investing in the current uncertain market (correction?) No clear direction.