It is hard to deny the importance of money in modern capitalistic life. More often than not, money is the carrot that is dangling in front of us, making us wake up at ungodly hours or rushing to appointments that we would rather not attend.

I reckon most people have resigned themselves to a lifetime of the above. Although I simply refused to.

And I always thought the option to Financial Independence, Retire Early (FIRE) is available to most residing in a developed country such as Singapore. Of course, I still earnestly believe everyone can start with the man in the mirror to consume less, improve their financial situation and save the Earth.

But the option to FIRE for everyone?

I am no longer so unequivocal in believing that’s possible for most, because I have come to understand that pursuing Financial Independence is a privilege. If one is not blessed with certain endowments, it’s really an uphill and unmotivated task.

I realise I am on this privileged path because of the factors below.

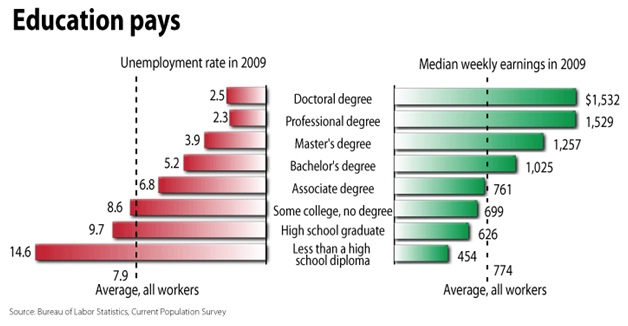

High Education and Income

It might not hold true for much longer but I am still willing to go out on a limb and expect the correlation between education and income to remain quite strong over the next two decades.

Unless you have other endowments like good looks, very thick skin and a more submerged conscience that enables you to do well in the service line or sales, more often than not, the odds are that you need to do well academically or at a specific skill to enjoy a high income.

The Mrs and I are academically inclined and consistently among the top 10% of our cohort in assessments and it was a big factor in helping us to collect above average paychecks in our early years climbing the corporate ladder. It continues to surprise me that the academic achievements in the past continues to pay dividends as just yesterday, I was able to earn $200 from a 1 hr 45 min lesson teaching A Math to a group of students.

If one is struggling to earn above three or four thousands a month consistently, it is really difficult to save enough to FIRE.

Excellent Health

I might not have ideal body composition (hey, but I am working towards it) but otherwise, there’s really nothing much to complain about my health.

If I were to suffer from some chronic or debilitating illness, I guess FIRE would be one of the furthest things from my mind. The priority would be to treat and contain the diseases, even if it entails spending a large sum of money.

Right now, we spend a very small proportion of our incomes on maintaining our health. Basically, just an Integrated Shield Plan, some vitamins and the occasional chicken essence. These savings are channelled towards investments which help to accelerate FIRE.

A higher quality of life is almost sure to result from having more liberty with the way I can spend my time. But if I don’t have the health to enjoy it, what’s the point of FIRE then?

In fact, one of my more immediate goals is to implement and get used to a system of healthier eating and sustainable exercising to complement my good health.

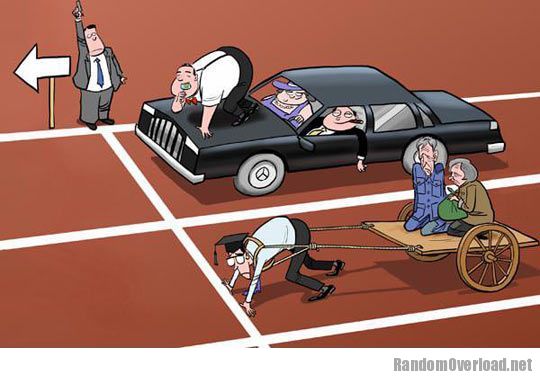

Favourable Family Background

Notice I did not write “advantaged”. If one is advantaged enough, he could FIRE the moment he is born.

But I also appreciate that I am not on the other side of the spectrum like a friend of mine. Although she earns upwards of $6,000 a month, she is a single child and both her parents are aged dependants. Almost half of her salary goes towards their living expenses and medical bills.

She had excellent grades in school and is doing pretty well in her career and is also blessed with good health thus far. But because of her family background, I honestly doubt she can achieve FI before she turns 45.

She had excellent grades in school and is doing pretty well in her career and is also blessed with good health thus far. But because of her family background, I honestly doubt she can achieve FI before she turns 45.

My Mum passed away when I was still in University. It actually took me years to come to terms with it and because I am somewhat estranged from my father, the only silver lining I can grasp is that I don’t have to contribute any allowances to my parents.

The Mrs’ parents are probably still earning a higher monthly income than the both of us and their retirement is well taken care of from close to 40 years of non-stop employment. Therefore, the Mrs only provides $450 a month more as a token/appreciation rather than to support them.

This allows us to accumulate our stash at a higher rate than many others.

Invest Early

Both of us started investing at 24 and by the time we turn 45, we would have invested for more than 2 decades, which gives our money quite a bit of a runway to grow and accumulate.

On the contrary, not many people bother about growing their wealth until their late thirties or even beyond. You might protest, but being a reader of this blog is already a statistical anomaly, so for a more accurate representation, just observe your friends, relatives and colleagues around you.

Honestly, if we were to stop injecting any money into our portfolio and assuming a conservative 5% annual return on $400,000 over the next 15 years, we would be closing in on $800,000 when we turn 45.

By investing early, by the time we turned 30, our snowball has already accumulated significantly and it is only going to grow bigger and bigger as it amasses more snow rolling forward.

But not many people have the money and the willingness to invest that money in their roaring twenties.

Discovery Of FIRE

Not many people come across blogs like Mr Money Mustache, Early Retirement Extreme and The Escape Artist in their twenties and to make it harder, even fewer would learn to appreciate them like I do.

Most dismiss these people as crackpots and tell themselves that they are not willing to deprive themselves of happiness and pleasure just so they can stop working in their thirties or forties.

Just because I idolise them because of certain worldviews and beliefs doesn’t mean everyone would. After all, even I have to admit that they are pretty extreme if we are comparing to the norms in society. Just like how a Paleo diet sounds to the Mrs who is a big French Fries and Potato Chips lover.

Once it appears too extreme and too different from the person’s current lifestyle, most people are simply not rational enough to give consideration to that suggestion. I know it because after years of procrastination, I finally started limiting my carbo intakes for a few weeks to test out a pseudo Paleo diet.

It’s not easy to discover FIRE and then embrace it. When faced with a potentially benefiting idea that threatens to upset your current lifestyle, unless it resonates immediately, it’s much easier to dismiss it than to bother experimenting with it.

The whole post sounds a bit pessimistic on the FIRE front and honestly, if one of the above factors don’t work out, FIRE could just be a pipe dream.

But at the same time, if you have the privilege of the above, there really shouldn’t be anything stopping you from attaining FI at an early age?

For those not as privilege, it is still possible.

But at maybe after the age of 55 to 60 years or even later.

They say, “It’s better late than Never”.

Hi temperament,

Yes, it’s not a race with others. Everybody has different circumstances and there’s nothing wrong with a preference to go at a slower pace too.

Completely agree that everyone has different circumstances and goals – life is easier for some and harder for others. That said, I’m quite inspired that there are some middle to lower income folks who have managed to achieve financial independence through sheer determination and hard work. These guys who have managed to beat the odds worked their butts off and lived extremely frugally for an extended period, and I find their doggedness mighty impressive (although I must admit this is not for everyone).

This is one of my favourites – an American who lived on $7,000 per year for 10 years: http://earlyretirementextreme.com/how-i-live-on-7000-per-year.html

Perhaps “Financial Independence, Retire *Eventually*” is the more realistic pursuit for most…

“But at the same time, if you have the privilege of the above, there really shouldn’t be anything stopping you from attaining FI at an early age?”

Actually, once one has been red-pilled to strive for FIRE, the accumulation phase becomes such a grind that semi-ER appears to be the more gratifying option. At least for me haha.

“If one is advantaged enough, he could FIRE the moment he is born.”

I know one of those! My uni coursemate instant FIRE upon graduation because her parents provided her with an income portfolio, cashflow from their family business, and rentals from property.

Can retire without financial stress is good enough

I think more higher-income people are becoming aware that having a high income stream is the biggest factor towards financial independence or even the ability to have a voluntary retirement. It definitely gives you options. Much has been said about things such as Mr Money Mustache’s early retirement at 30 yrs old.

E.g. http://www.flannelguyroi.com/dirty-little-secret-early-retirement/

Even PAP is becoming more forthright about it now (they probably knew about this long time ago, pretty commonsense right?!?). Jos Teo or wazit Indranee who recently said that it’s more important to find ways & means to ramp up low income earners’ incomes. This when responding to reporters’ questions regarding the 30% increase in water taxes. A tacit admission that there are Singaporeans earning too little in high-cost Singapore? But they really need to update their policy — they still term $2500 *gross* salary as middle-income… .

Of course the 2nd biggest factor for FI is save:spend ratio. But in the first place if your household income per capita is $1500/mth or even less, then it’s very hard to make meaningful contributions to retirement savings.