Like most hot-blooded young men, I was first exposed to the insurance industry’s sales tactics at the tender age of 19. While I was waiting for my bus to get to camp at Pasir Ris MRT station, a good-looking female insurance agent approached me, wanting to share with me the benefits of a good insurance plan by arranging for a one-to-one session.

That proposition proved to be irresistible. I handed out my contact information, and the rest is well, history.

Besides buying a conservative endowment plan (which I had liquidated at a small loss many years ago) during those NS years when I first experienced drawing an income, I had also bought this Investment-Linked Plan from AIA called the “Achiever” plan. It was sold to me as a savings plan, where I would set aside $100 each month, 50% invested in China funds and another 50% in India funds. 15%-20% returns were touted back in the roaring mid-2000s when China and India were booming and I was hooked.

It had seemed such a good use of my money then. After all, I was investing in some hot growth funds instead of squandering it away by opening bottles in clubs or purchasing a PSP. But alas, all I was doing was fattening the wallets of that pretty insurance agent and of course, AIA. Here’s the reasons why this policy was such a lousy deal for me:

====================

1. Failed to recoup my capital

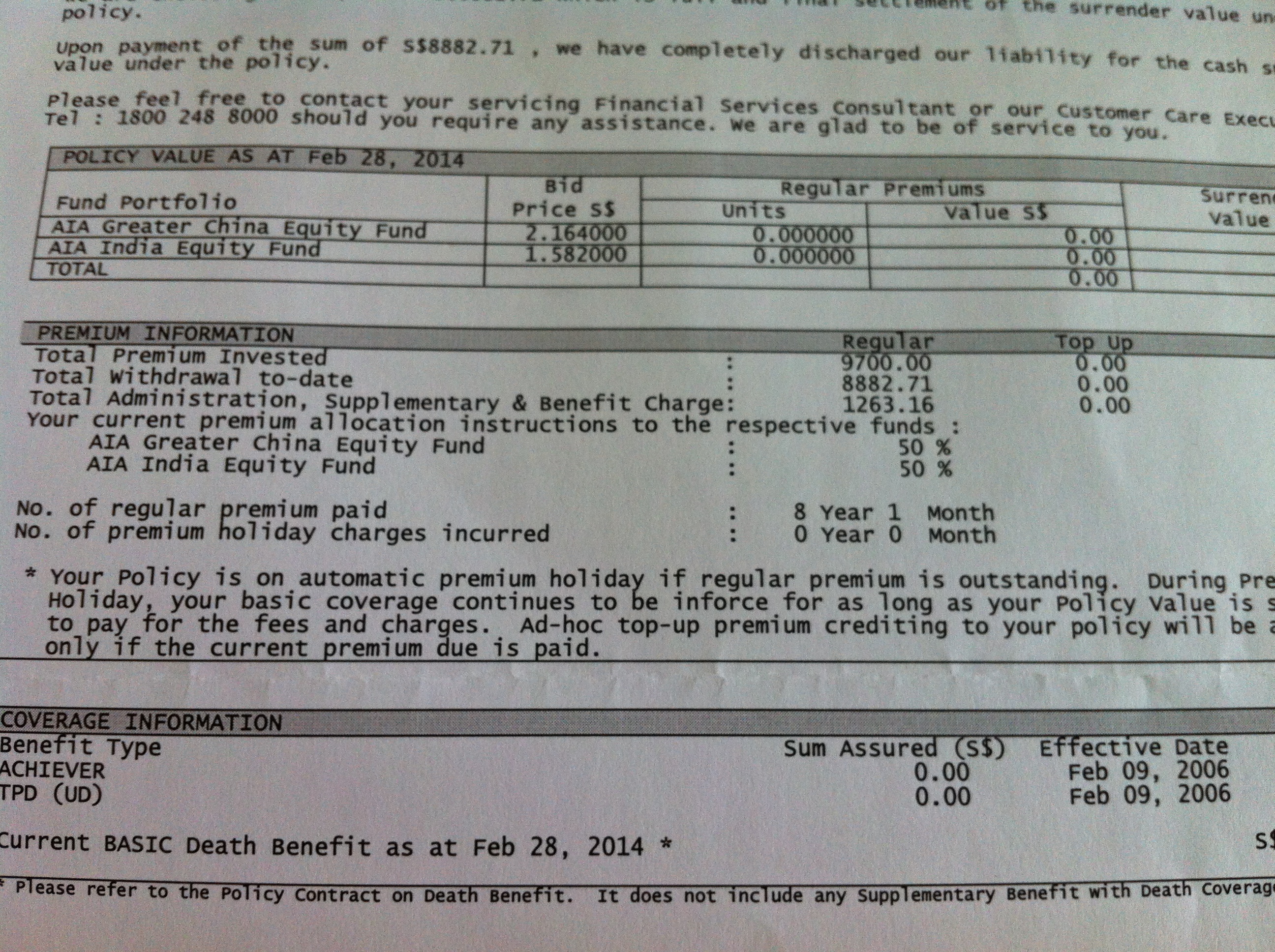

By the time I surrendered this policy in Feb this year, I had been holding this policy for 8 years and 1 month. That’s $9,700 poured in. But the withdrawal value was only about $8,900! Even if I had just put the money under my pillow for the past 8 years earning 0% interest, I would have been better off with an extra $800.

Ok, this Achiever Plan did come with some insurance coverage, so you might think that a significant amount could have gone to cover those premiums. But then, 8 years ago, I had opted for the lowest insurance coverage available for this policy, which was $6,000. This is less than 20% the amount covered by my Dependents’ Protection scheme (DPS). And well, DPS only sets me back by $40 a year. I shall rest my case here.

2. Hefty Expenses

This also brings me to the next point. By the time I had surrendered the policy, it was stated that I had spent almost $1,300 on admin, supplementary & benefit charges. It’s obvious the premiums for the insurance coverage would not have exceeded $300 over the entire 8 years, which leaves us with $1,000 unaccounted for.

Wait. It’s actually accounted for since that’s probably the admin and distribution charges, which are just nicer terms for money that goes to AIA and the pretty insurance agent’s and her supervisors’ pockets.

This plan was very likely a winner for both company and agents since Mrs 15HWW also bought the exact same product as me a few months later. You could imagine my shock and disdain when I found this out about 5 years ago. I guess the Achiever Plan really lived up to its name, “achieving” a lot for the company, at the expense of policy owners like me.

3. Opportunity Costs

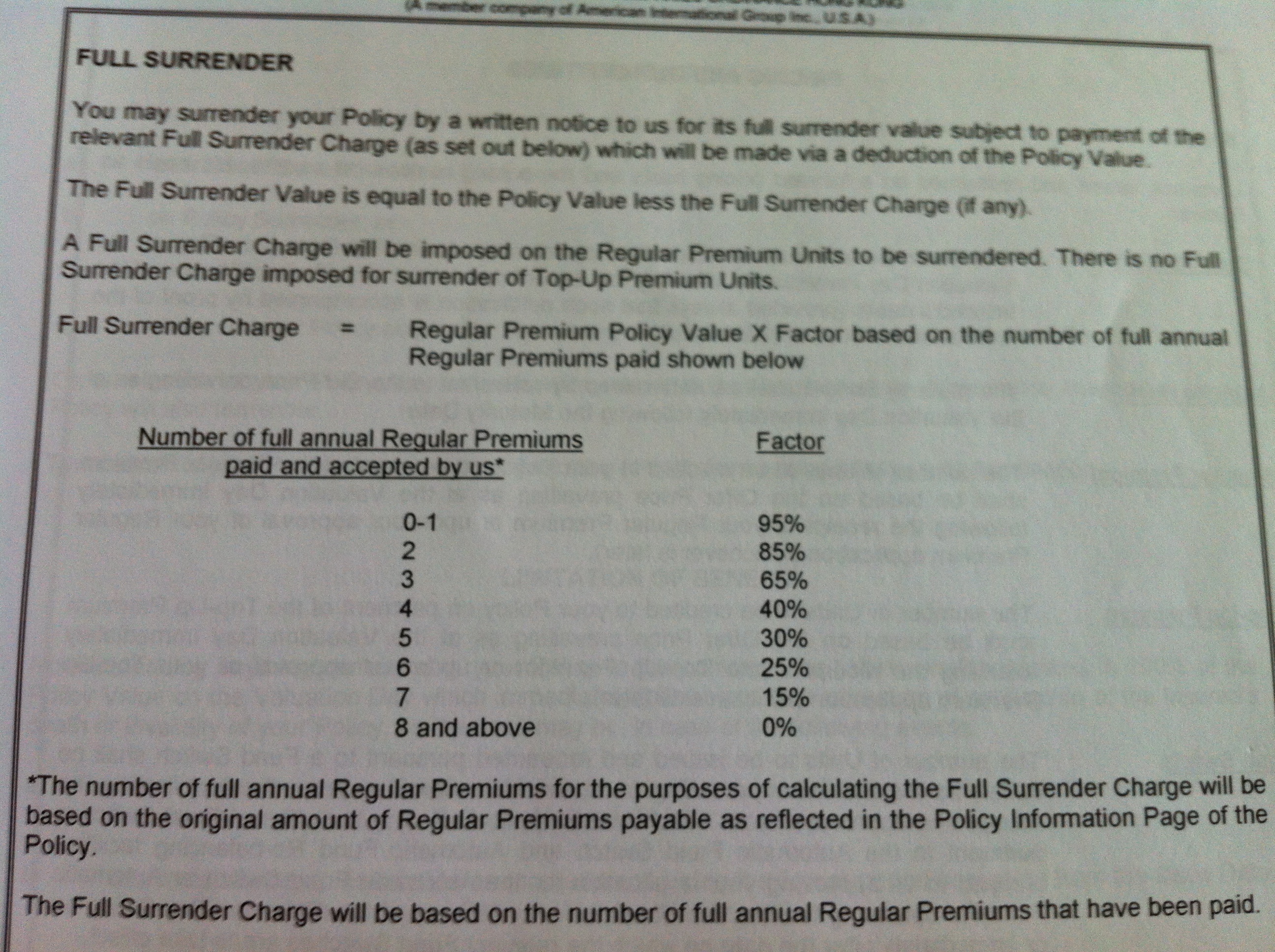

There was a wonderful pre-commitment device built into this policy (yeah, I am being really sarcastic here). If I had terminated it in Year 4, AIA would impose a 65% charge on the value of my investments and even in Year 8, the charge was a significant 15%. The hefty penalties meant I really had little choice but to keep the policy going even when I knew this whole thing was a mistake early on.

If I had access to that few thousand dollars, there was a good chance I could have started my investment journey earlier in 2008 or 2009 and caught the bottom of the stock market cycle? So my loss could really be in the thousands, much higher than the $800 stated earlier.

====================

Lesson learnt? It’s important to know if that other person’s incentives and motivations is aligned with your well-being. That’s why I am much more in favour of a fee-based model in the insurance industry compared to a commissions model. As what Buffett famously said, you wouldn’t really want to ask a barber if you need a haircut.

Long time ago, I wrote about an article on how I don’t trust financial advisor because their objectives are not aligned to our needs. Got a lot of brick bats for that. Haha but I guess for your case, you got hooked by the lady.

Lately I wrote an article on the importance of having term policies. Check it out in my blog, SG Wealth Builder. Many Singaporeans like to buy expensive whole life and investment policies but they don’t realise these are not pure protection plans and does not serve the purpose of protecting our assets at all.

Hope our blogs can help to educate Singaporeans on how to manage their money better.

Regards,

SG Wealth Builder

http://www.sgwealthbuilder.com

Hi Gerald,

I guess at that young age, I was even more thin skinned and just couldn’t bring myself to reject a person. I already had some concerns even then but since I wasn’t of age to set up a CDP account then, I caught the bait. Oh well.

Agree that for money-savvy people, term insurance is all the protection we need.

I think the key problem was the agent didn’t explain the policy properly! Achiever is a long term plan which for people to invest for more than 15 years. If they really read the terms and know how to use the adventurous portfolio and switch funds function to manage the policy, you will see the figure be much different on nowadays 2021. I’m so sad to see lots of unprofessional insurance agents so irresponsible and even wrongly to explain to the customers without properly knowledge them. I’m glad that my ILP policy return running well for the passed 15 years and I’m looking for a better wealth grow for my retirement.

omg… i also bought this AIA achiever plan… totally regret cuz soon after i bought, it was financial crisis… haiz and it is only my 5th year going into the 6th… still having a loss of 2k+ but i cannot do anything but to hang on… >_<

Hi Melting_starz,

Look at the silver lining? It’s just another 2-3 years before you can get your hands on the money and you will probably not go near such plans again.

I also regret having that policy as I just review my policy I still loss out more then 2k and worse of all, the person who get me to buy is my previous manager. Because of the relationship, I never rejected him.

By the way did you review before AXA flexisaver (Also ILP)? It seem to have some good saving element and with an average growth of 13% (Fund: Fortress A) for the past 11years. Would be nice if anyone can give me a feedback.

Do not buy ILP without knowing the funds that they are going to, as well as the charges. AXA flexisaver is not the best ILP, but still better than this Achiever product. The downside is that flexisaver does not give you a high insurance coverage.

To me, insurance is still important, especially health insurance, as for the life insurance, there are too many gimmicks being thrown in recently and kind of agreed with Gerald that simple term life policy does the trick!

Enjoy reading your post!

Hi Richard,

Insurance was a concept that was designed to improve one’s utility, especially when protecting against catastrophic losses. Good intentions but some have taken this useful concept and morphed them into products whose main objective is to generate sales and commissions. Urrgh…

Agreed, the whole payment structure of insurance has brought along many agents who are in the industry for all the wrong reasons. However, good agents still exist out there and this shouldn’t be a reason to not get covered at all (as most people are thinking now).

However, the fee-based system has been tried, but has yet to see results. I guess that’s why they’re sticking to the old system of compensation for agents..

Hi hww

Like you, I was caught offguard and ignorant when I signed up for my unit trust insurance when I started working. But it does give quite a good coverage should something happen. Of course 5 years down the road I decided to cut the loss short knowing that I could invest my money better. The thing with these type of insurance is probably 5 to 10 years are considered short term. Should you wait another 5 years you probably would get more than you would have put but is the return great? Thats ourselves to ask for…

The admin fee of the ILP accounted to almost 14% of the total premiums paid. Scary!

One of the major issues in this case is the way this policy was “mis-sold” as an investment vehicle. I would use the analogy of a doctor informing the patient that Panadol can be used to cure cancer. It is setting the wrong expectation for the patient and likely to leave him disappointed. These kinds of policy have their part to play in the overall insurance portfolio of a person, but is dependent on the specific needs and circumstances of the person.

Hi John,

I agree with you and I think that the problem with the industry is that the bulk of the transactions consist of “mis-sold” policies.

I think it’s all one-sided. I have a total of 5 Achiever Plans. All made money. I think it’s just that you dun go for long term. And as compared to stock market, I think maybe we could lose that $800 easily in a day.

Achiever is a good plan, just that you cannot be doing up your savings in a short term. Its a minimum 8 years plan, doesn’t mean you take it out on the 8th year. It suppose to continue after that. And also do not say you put the money under your pillow. Without a plan that offers penalty, you can’t save up these $9k also. Moreover, what savings plans are there in the market that is such a short term without hefty penalty charges. The idea of penalty charges is to make you keep saving, not into the pocket of companies… Even though it is, it depends how you see it. If you can appreciate its benefits, it’s a good plan.

Hi SK,

Wow, 5 Achiever Plans. Happy for you that you made money for all your plans.

To be honest, I don’t think 8 years is exactly that short term. And I feel that the AIA Achiever Plan is riddled with all sorts of expenses. I have never changed my allocation over the 8 years and it was 50% in some India fund and 50% in some China fund.

If I had invested it in some ETFs that were based in HK, I would have ended up with a much higher amount after 8 years.

For people who can save up $10k and invest it themselves (think I have shown it), I really think they can do much better than this Achiever plan.

For example, I would really be much worse off today if I had put in $1000 a month into this plan instead of investing on my own.

Hi, I’m so thankful for your post, as I am now reading my husband’s AIA insurance letters (similar to yours) and thinking this was a big mistake. I think he was also young when he bought this Achiever plan and he’s so busy with work now he hasn’t had time to properly sit down and manage this. At 7years and 11months now, I think it’s time to surrender at a loss.

Having said that I am very interested to hear how SK has made money from this or if anyone else has. For my husband’s policy, the surrender value is $13887 but premium invested is $15300, admin charges $1712.79. It seems so wasted that he doesn’t even break even. Should I get him to surrender now or like SK said, is it meant for longer term?

I wonder how many other young souls out there are getting conned into this and because it’s automatic payment, they probably forget about the payments altogether – not knowing that they are losing money.

Hi Michelle,

Firstly, apologies for the very late reply.

Pardon me, but I doubt holding the policy longer would help matters. The admin charges would continue to accrue and they make up a large part of our returns. If I am not wrong, there’s no penalty once the policy is in place or 8 years.

When my wife’s policy expires in a few months’ time, we are definitely going to terminate it.

There are many that advocates automation in our lifestyle. I personally enjoy some of the convenience automation provides but I have to admit automation does make us too complacent in some of the most important aspects of our life.

i have the same plan, dosent seem to make money. I was at the verges of surrendering, but an AIA agen came knocking in my door to seel insurance. I vented my anger on him, as i am loosing money.

He begged and was persistent to let him look at the investment. He did some twitching and brief me about how fun switching is usefull at this kind of moment.

Truthfully, the investment seems to be going up, its was $18966 in december 2013. He just updated me few weeks back that the price i can surrender now is $23179.667….

U guys might want to ask your agent about this.

Hi Mike,

Thanks for your advice.

Both of us terminated our AIA plans once we hit the 8 year mark and the Mrs actually did it as recently as half a year ago. She actually made a very small profit after the Chinese market surged in the middle of the year.

I guess perhaps that could have also influenced the surrender value of your policy?

bought an ILP achiever plan with AIA for exactly 7 years.

total premium pay: $10500

current value: $8523.53

charges: $1275.81

1)What is the year that i could surrender without penalty? i saw in the latest statement that the current surrender value is $8523.53 which coincide with my current value. So does that mean that if i surrender now i can take back the full value without penalty?

Read in policy plan mention that 8 years of full premiums paid then the surrender factor would be 0%

2) According to the projected chart provided in the policy plan, the projected non-guaranteed value at 7th year coincide with the current value of $8500. So does it mean that it might hit the projected non-guaranteed value in the long run & possibly make money..

Hi jamesz,

Best is to check with AIA or your insurance agent.

For my plan, I really had to pay 8 years of full premiums to surrender it without a penalty.

I am not sure if it will make money in the longer run but do take a look at the expenses and see if it’s worth it relative to other investment products out there.

Hope my reply helps. =)

Now is my 7th year in my 8-year plan. I paid the remaining 1 year in advance (switched monthly payment into annual) so I can withdraw my money without penalty (as per my agent)

Hi Kei,

My wife also has this plan and there’s still a month to go before we can terminate it. Paying in advance is a good method. Maybe we should have done that when the China market was frothing so we could liquidate at a good price. Aargh…

I am in the midst of ILP withdrawal. How long is the processing time? I hate calling the hotline, its just a waste of time. The call center staffs doesn’t know anything about everything!

Hi Kei,

If I don’t recall wrongly, they sent the cheque within a month? I think you just have to sit tight and wait for the proceeds to come in.

If I am not wrong, ILP does not have any guaranteed value and depends all on the fund prices? Recent big event like China devaluating their currency is causing all fund prices to drop, thus the drop in surrender value?

Hi CS,

We will be able to surrender the Mrs’ plan soon and what you have mentioned is likely to have an impact.

But another bigger impact could be the high admin fees that the ILP charges.

Hi,

Do agree that admin charges are high and the insurance elements in the ILP will be increasing exponentially every year. Regular premiums policy from insurance companies must be sold on protection, not investment.

If looking for investment, should be buying single premium investment with no insurance elements. Thus costs will be low.

I think people who are holding ILP for 8 years to not surrender first and wait for 2 – 3 years more. I know you will still be paying, market is dropping. 2- 3 years when the equities market recover, and your surrender value is higher than what you have ploughed in, then you sell. Buy low sell high yeah? Just dont waste your money.

CS

To add on, consult your agent, or go for a second opinion.

Googled for AIA Achiever and came across this post…invested 16.2k so far coming to 11 years (10 years 10 months to be exact) ..now looking at 11.3k ..kinda sien…31% loss..

After last fund switch in late 2007 I just let it idle and never monitor

– 40% Greater China Equity

– 40% Emerging Market Equity

– 20% Global Resources

Now still thinking to continue pump in monthly $125 after changing to below split praying for market to recover or bite the bullet and surrender the policy…any advice?:(

– 40% Global Healthcare;

– 40% Regional Fixed Income;

– 20% Greater China Equity

Hi Eugene,

I am not sure if I am in a good position to offer any advice but I can only say that I have since terminated both the wife’s plan and my plan. It was a no-brainer for me once we went past the 8 year period when no penalty was imposed. The admin charges and fees will likely reduce the potential returns going forward.

Hey, I was looking at this ILP called Optimus by AXA, recommended by a friend, and wondered if it was a good product. Advice pls.

Am aware that it requires a minimum of $1,500 per month.

Thanks!

Hi SJ,

Wow, $1,500 a month. Unless you earn a very high salary, that’s alot taken out of your disposable income.

Hi sir,

ILP policies are designed to breakeven from the 11th-13th year depending on the premiums you put in as compared to traditional policies which has a breakeven of 35years for the same premiuns. In my humble opinion i think the agent has actually mis explained some parts of the product to you. It would be great if i could actually meet up with you to have a chat regarding comprehensive financial planning which i hope could ultimately give u a clearer picture on the benefits of insurance. Btw I am a financial planner from great eastern

Hi GE LIFE,

Thanks for your offer and I would definitely consider your services if I intend to sign up for any GE policies/plans.

Hi.im a axa financial planner . In my pov please dont buy any ilp unless you know the agent will be doing lots of homework for the market or you ownself will be doing. If not the charges incurred in ILP is not worth the money.

Sorry to hear about your plight. When I was about 15 years old, I already heard about NEVER to buy insurance unless one is sure that he/she will meet with accident or die early. It’s easy to pay them (insurance companies) but it’s very difficult to gain from them. I might as well leave my money to rot in the bank (or buy gold from UOB) than to buy any insurance.

Hi Steven,

I guess the most painful thing about insurance is that one rarely buys it. They are mostly sold to.

Some annuity plans that yield 3-4% could actually be useful for specific individuals.

Just surrendered this AIA Achiever Plan after holding it around 10 years. Total premium paid = $12,200. Surrender Value = $8,200.

Total Loss = $4,000.

I am not sure whether $4,000 is considered loss or not, as I did add on TPD and Critical Illness Rider of $100,000 for this plan in the past. Maybe the lost is just around less than $1,000 as I computed my average unit buying price is at $0.9 and my surrender unit price is at $0.836

What I don’t like about this plan is hidden fee which seems very high

Guys, in the first place.. You are combining an insurance plan with investments which is not really a good idea. Life insurance have mortality charges and it eats up your investment as you age. Eventually the mortality charges gets so high that it exceeds your investments returns.

Always get a life insurance without any fanciful complications, in your case, it is investments. Having said that, AIA and Prudential does have a pretty good pure investment product that are managed by professional fund manager and I do have clients whom are making profits from this investment tool.

If you are only into short term gains, then an endowment plan should work for you, but life insurance and investments are always for Long term. Purpose is to grow your wealth and preserve your wealth.

Personally, I am from Prudentail, and by saying the above, I am not siding anybody, just saying from experience and knowing the benefits of getting insured against uncertainties. Insurance is to protect you against serious illness and disability, rather than a tool for you to gain investment profits although for your case, it is an investment linked insurance which I really don’t recommend to any of my clients at all as it is only suitable when you get it at a very young age. I got it for my own child with $100,000 coverage.

Last but not least, it is always advisable to stay invested in the market rather than timing the market. You never know for sure when investments will go up or down.

A few question probably we can ask ourselves or the financial planners;

1.For investment product, there are a few platforms(i.e. Fundsupermart, Dollardex, Philips Poems, etc) where we can buy and access the unit trust/funds ourselves, and it is probably more cost effective.Why do we need to invest via an insurance companies which their main purpose is suppose to be providing protection coverage.

2.Some of investment products(unit trust) provided by the insurers, the underlying fund is also from the usual fund houses(i.e. Aberdeen, Fidelity, Lion Global, etc) which can be bought directly from the platforms as shared earlier, why should we pay additional layers of charges, to the agents, policy fees, insurers, fund houses and the underlying fund expenses ratio.

3.Do the financial planners/advisers/agents really a system to help each and every client of his/her to monitor and manage their investment portfolio during the time they stayed in the market to justify the commission paid to them, or is it just to get the policy holder hooked up with the investment plan and ILP and forget about them and moving on to get another client onboard. Are they themselves in the 1st place investment savvy or just sales savvy?

4. The investment product via insurance may be making profit, but rising tide raise all boats. Could we obtain higher profit if we invest via a similar or comparable product with low charges if one were to invest themselves, i.e. ETFs?

5.Will the planners in the 1st place share the available options in the market, or solely just marketing his/her own products?

Just thinking aloud

Hi guys,

1) An investment linked policy is not an investment tool…

its a Life Policy meant for Protection with some investment element in it..

So i don’t think its comparable to investing in the stock market.

This is like buying a rice cooker and complaining that it cant wash your clothes.

2) It’s definitely not a good protection plan for those who insist in buying term and

investing the rest… therefore not recommended for people who love to invest their

own money.

3) It’s usually mis-sold by unethical agents as investment or savings plans.

However, if a person buys an ilp as a form of protection and wish to have some form of

investment and do not invest on their own, an ilp can be a good plan suitable for

him/her. It all depends on each individual needs.

Therefore, for those who have been mis-sold an ilp as an investment tool, the few

options for you to choose from is:

A) Surrender the policy if you feel that you can invest for higher returns elsewhere

B) Keep this policy and go on premium holiday, which means that the money in the

policy will be used to pay for the insurance charges, effectively changing your ilp

nto somewhat a term plan

C) Continue paying this plan and keep it as a protection plan which has some cash

value at the end of the day, if you do not actively invest on your own.

Please inform your agent that you wish to increase the coverage if the coverage is

very low like $6,000-$10,000. It does’t makes sense to have only $10,000 coverage.

Usually you can increase your coverage up to $50,000 to $100,000 without

increasing your premiums.