This is the 4th consecutive year that I am updating our net worth on this blog. And as usual, the result surprises on the upside. Cue one of my favourite gifs…

The snowball is finally starting to accumulate, grow bigger and roll faster down the hill.

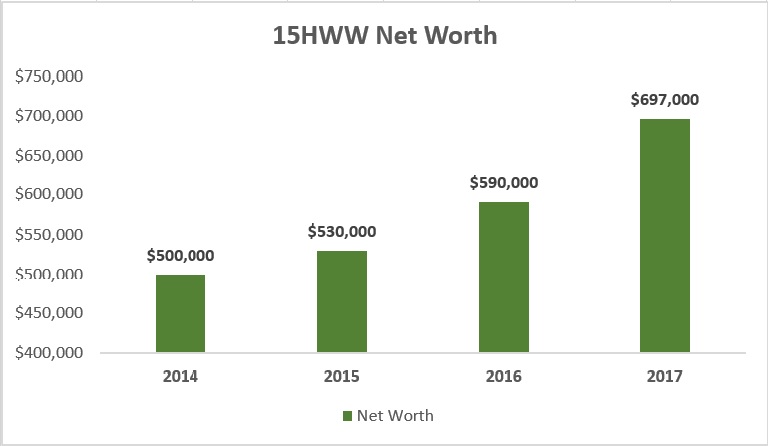

Our net worth currently stands, at $697,000. This represents an incredible $107,000 increase as compared to 2016.

The main contributor is still the savings from our income ($65,000). The bullish stock market has also contributed significant capital gains ($32,000) while dividends, bond coupons and interest added another ($10,000).

I have also simplified our net worth into 3 main categories for easier visualisation and tracking.

Equities ($252,000)

Local Equities ($190,000): Besides the local stocks in the portfolio, it also includes purchases in our POSB Invest-Saver.

Foreign Equities ($62,000): Comprises Berk B and 4 other HK stocks. This is still a relatively small exposure of about 25% of the entire equity portion.

Cash, Bonds & Commodities ($242,000)

Cash ($129,000): SGD deposits in six bank accounts along with about $15,000 in foreign currencies.

Bonds ($78,000): The CPF Ordinary Account balances make up more than half of our bond portfolio. The other portion comes from our Singapore Saving Bonds (SSBs) and $22,000 worth of FCL bonds.

Commodities ($35,000): No cryptocurrencies. I might be missing either the opportunity of a lifetime or one of the biggest crashes ever. It’s really just a conservative mixture of Physical Gold & Gold ETFs here.

Home Equity ($272,000)

Home Value ($500,000): This BTO flat that I have lived in for more than 4 years (older than this blog) will reach its Minimum Occupation Period (MOP) in a couple of months time. Although I believe the houses in my estate will fetch more than $500,000, I have decided to be conservative until some resale transactions are lodged on the HDB website.

Outstanding Mortgage Loan (-$228,000): This home loan is being chipped away very very slowly. And why not, since my interest on the debt is much lower than 2%?

Other Liabilities (-$69,000)

The amount of my siblings’ funds parked with me has reduced by quite a bit as I have started returning my sister’s funds back to her. The Mrs also plans on returning her school fees to her parents and the proceeds of an endowment plan that her parents had bought for her.

So, would a net worth of $700,000 enable us to retire?

Probably not, unless we uproot to a place like Chiang Mai and perform some geographical arbitrage. This isn’t what we really desire but it’s still good to know that we could pursue an option like this if push comes to shove.

Most likely though, both of us will continue putting in more heart, sweat and tears into our trade. That should help to push us comfortably forward in our journey towards Financial Independence. And yes, looking forward to breaking the $800,000 mark next year.

Till the next update in a year’s time.

You can refer to the networth updates in the previous years here:

Our Net Worth Update – 2014

Our Net Worth Update – 2015

Our Net Worth Update – 2016

wow that’s some impressive figures! Are you planning on cashing out of your BTO unit? Perhaps selling it and getting another?

Hi Kate,

I am sure you and Dave are likely to arrive at a similar or even higher figure?

Unlike most others, our figure is likely to be inflated by the “home equity” portion. We are quite flexible on the home part and definitely open to applying for a new BTO and selling our current place if the stars align. =p

Ehh … if 2nd BTO, don’t forget about the resale levy — which is usually more than the cost of an average renovation.

In the old old days, we didn’t need to pay resale levy if upgrading to new bigger flat e.g. 4rm to 5rm or 5rm to Exec. Those were the “asset enhancement” and govt-encouraged upgrading years. Imagine ministers today going on TV to encourage people to buy bigger houses. The Roaring 80s! LOL!

Hi Sinkie,

I guess a 2nd BTO is also about renewal of lease and a move from a flat with aging renovation. If can make money, good, but that’s probably not the main aim.

With the flats being built getting smaller, I doubt any minister will go on TV to talk about bigger homes anytime soon!

http://www.creditsavvy.com.sg go for this talk it only cost you 2 hrs of your time and I am sure it will change the way you look at ptoperty investment.

Hi See Hwa,

Thanks for dropping by and your recommendation.

I do have a small hope of upgrading to a private property some time down the road eventually. But two private properties is probably stretching it and taking on a whole lot more of risk that I am prepared to bear.

Thanks for the update.

Congrats on the progress.

“The CPF Ordinary Account balances make up more than half of our bond portfolio” – does this mean that you invested CPF OA funds in bonds?

Also, why don’t you include your other CPF balances in your networth?

Thanks and jiayou!

I think m15hww probably meant his bond-like fixed income portfolio since CPF gives out fixed returns and the principal is safe. I’m not sure if funds in the OA can be invested in bonds?

Hi JF,

Mr C is right. CPF funds are bonds to me and it actually does not really make much sense to invest CPF funds in bonds. Likely the returns are lower.

I am actually not inclined to include CPF funds due to the long horizon (~25 years) before the funds are liquid. CPF OA is slightly different since it can be used to pay down the mortgage and I have included the outstanding mortgage as a liability.

Right. Concur with you both on viewing CPF funds as bonds. I treat the cash TOP-ups to my CPF SA as bonds in my portfolio.

Thanks for sharing your thoughts – gambatte! =)

65k is a lot of saving. And with 43k expense tracking. You are making more 100k cash a year. If consider cpf, then you are making 130k a year. Looks like tution is a quite good paying job.

Congrats.

Hi Awksu,

Actually, this is a combined update and includes the Mrs’ portion too. So you can divide the numbers by two.

There’s probably a bit of double counting since I always include the mortgage payments as an expense and the payments help to reduce the outstanding mortgage so part of the expenses goes towards savings. Pretty convoluted.

Great progress! Your portfolio growth demonstrates the value of spending less and saving more which is a sure and steady way to FI. People tend to focus on investment returns whereas actual portfolio growth in the initial years is probably derived more from savings, until the portfolio reaches a certain size.

Hi Mr C,

Yes, even at this stage, the organic growth of the net worth is dwarfed by the savings contribution. But moving forward, it’s likely savings will play a smaller role as we are likely to earn less and spend more?

I think yours and Ms K’s portfolio should have reached the stage where the organic growth is very impressive by itself!

Woah. That’s impressive. 700k at the age of 31. Wondering if CZM and I can achieve that when we are 31… lol.

Hi KPO,

Honestly, my bet is your are likely to exceed it. After all, your medium term goal is a $500k portfolio and if you achieve that, $700k should not be difficult if we add in home equity and your CPF funds.